Everyone’s Competing, Nobody’s Cheaper: The Marketplace Illusion

A free market is a machine that turns private ambition into public comfort, as long as competition stays real and entry stays open

In the clean textbook version, firms do not keep extra profit for themselves over time, the market invites new entrants until economic profit is pushed down to zero, and the long-run gains flow into better prices, better service, and more choice for everyone else. (OpenStax)

That sounds almost sentimental until you remember the catch, modern markets often look open on the surface while running on hidden levers, default buttons, rankings, switching friction, and rules that punish sellers for trying cheaper routes.

PROLOGUE

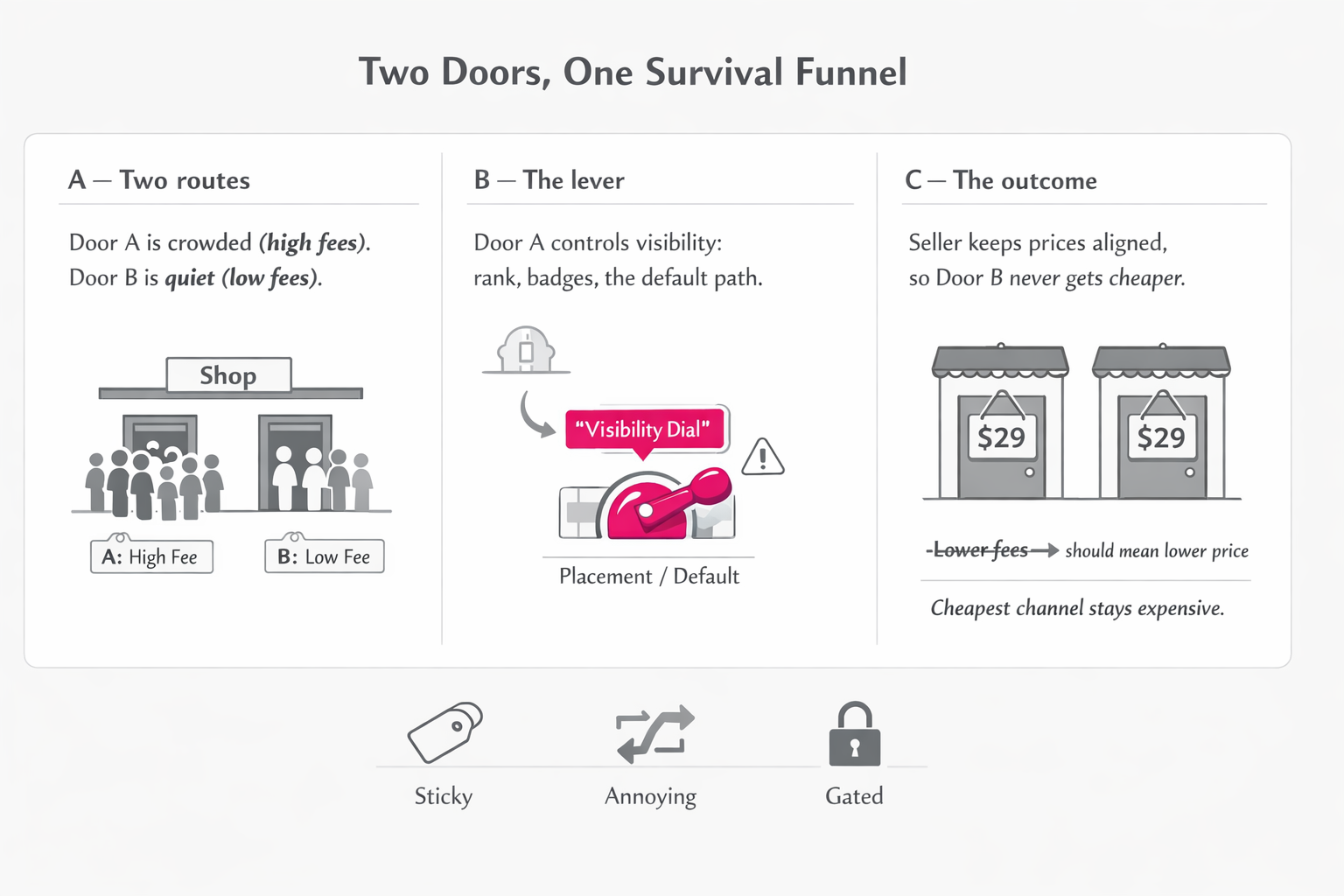

Picture a little shop with two doors. One door opens onto a busy sidewalk where everybody walks, the other door opens onto a quiet side street where rent is cheaper and the air feels calmer. The landlord owns the busy sidewalk, he owns the lighting, the signs, and the little arrow that says “this way,” so he never needs to shout.

Now imagine a rival street manager comes along and offers the shopkeeper a sweeter deal, half the commission, lower rent, fewer hoops. The shopkeeper wants to say yes, he wants to lower prices on the cheaper street and grow it, because that is what competition is supposed to look like. Then the shopkeeper remembers the busy sidewalk, and the fact that his survival depends on being seen there.

So he keeps his price high everywhere, and he calls it “consistency,” and the market becomes polite in the way that makes consumers pay more.

Example

A merchant sells a simple product, nothing fancy, nothing rare. The smaller street offers lower fees, so the merchant could cut price there and still make money. He refuses, because one quiet penalty on the busy sidewalk, a worse placement, a lost default button, a slower path to “add to cart,” would erase more profit than the lower fees could ever create. The cheapest channel stays expensive, and the expensive channel stays dominant.

What to watch for

- Prices look strangely similar across many sellers and many sites, even when fees differ

- Sellers talk about “not risking visibility” more than they talk about manufacturing cost

- A single doorway seems to decide whether you exist, even when nobody says it out loud

- Rival channels struggle to grow even when they offer sellers better terms

- Discounts feel rare, timid, or hidden in awkward places

- The market feels busy, yet price pressure feels weak

🔽 Click to Expand: The Economics

This story is a simple way to describe a classic mechanism, a platform that controls the demand funnel can shape behavior without issuing explicit commands. The key input is conversion elasticity, meaning how much a seller’s sales change when they lose a default position, a badge, or a ranking slot. When that elasticity is high, even a small probability of losing placement becomes a major expected loss, and sellers start acting defensively.

In the textbook benchmark of perfect competition, free entry and exit erase economic profit in the long run, because any extra profit invites entry until price is driven down to average cost, including the opportunity cost of capital and labor, which is why economists say “economic profit goes to zero.” (OpenStax)

In platform markets, the same entry logic can be blocked or weakened when access to demand is mediated by defaults, opaque ranking, and enforcement discretion. The market can still look crowded, many sellers, many listings, many offers, while behaving as if entry is constrained, because visibility is scarce and governed. Competition becomes a fight to stay eligible rather than a fight to lower prices. This is one reason modern competition policy discussions focus on gatekeeper power, platforms can tilt rivalry through conduct that raises rivals’ costs, increases switching costs, or makes multi-homing unattractive, even when “nobody is banned.” (OECD)

Signals that support the story include a price convergence pattern that does not match cost differences, sharp sales cliffs tied to default loss, and weak pass-through from lower-fee channels into lower consumer prices. Signals that weaken the story include stable visibility after off-channel discounts, durable price dispersion aligned with fee differences, and evidence that rival channels can scale by offering lower fees that translate into lower prices.

Key terms

- Economic profit, profit after all costs including opportunity costs, this goes to zero in long-run perfect competition (OpenStax)

- Normal profit, the baseline return needed to keep resources in the market, included in costs in the economic sense (OpenStax)

- Conversion elasticity, how strongly demand responds to visibility, defaults, and ranking position

- Expected loss, probability of penalty times the damage if it happens

- Multi-homing, sellers or buyers using multiple platforms at once, a core condition for competitive pressure

- Raising rivals’ costs, strategies that prevent competitors from winning by being cheaper or more efficient (OECD)

PART I — REAL COMPETITION

A real free market feels like a place where nobody gets to relax. If someone tries to raise prices without offering anything better, someone else smells the opportunity and steals their customers. If someone gets lazy on quality, someone sharper shows up with better service, and the lazy one either improves or shrinks.

In a truly competitive world, profit behaves like ice on a warm day. You can hold it for a moment, maybe even enjoy it, then the room fills with copycats, newcomers, and better deals, and that extra profit melts into lower prices and better treatment for the customer. That is the whole social bargain, private people chase gain, and the consumer ends up with most of the benefit. (OpenStax)

So the question is simple: do you see the pressure? Do you see prices respond, do you see new entrants grow, do you see real choice, do you see bad deals punished? When you do, you are watching competition.

Example

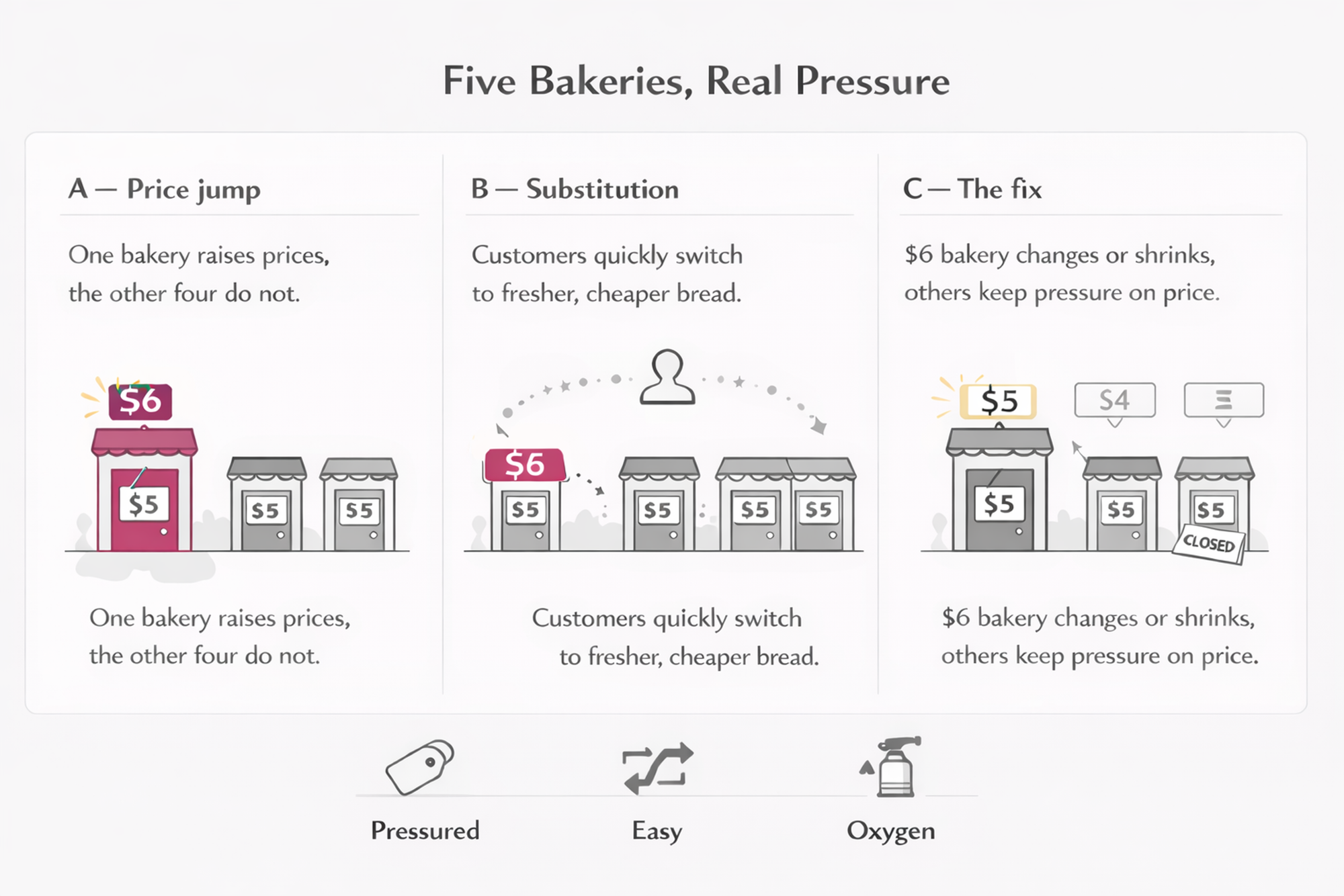

A small grocery street has five bakeries. One bakery raises prices because it feels popular, the other four respond with a special, fresher bread, longer hours, better service, and the expensive bakery loses customers the same week. After a few months, the pricey bakery either improves, changes its niche, or closes. That is the market doing its job, it is not personal, it is pressure.

What to watch for

- Prices fall when costs fall, and they rise only when something real improves

- New sellers can enter and grow without needing a special relationship with a gatekeeper

- Consumers can compare options quickly, and the “best value” can win

- Sellers can use multiple channels without fear, and discounting is rewarded, not punished

- Quality competition shows up as real improvements, delivery, service, reliability, transparency

- Firms complain about rivals undercutting them, because rivalry is active

🔽 Click to Expand: The Economics

The clean benchmark for “free markets” in Econ 101 is perfect competition, many firms, similar products, price-taking behavior, and free entry and exit. In that benchmark, long-run equilibrium pushes economic profit to zero, because any above-normal return attracts entry, which expands supply and bids price down until it equals average cost. (OpenStax)

This “profit equals zero” line is often misunderstood, it refers to economic profit, not accounting profit. Economic profit subtracts opportunity costs, including the normal return needed to keep capital and labor in the industry. So zero economic profit still means firms can be healthy and stable, it means they cannot keep persistent extra rents without inviting entry. (OpenStax)

A practical competition checklist is outcome-based, it asks what the market produces. Price discipline means markups are constrained by credible substitution and entry. Quality rivalry means non-price improvements translate into share, without being dependent on paying “access rents.” Contestability means entrants can reach buyers at scale, and multi-homing stays viable, buyers and sellers can switch or split activity across channels without large penalties. Choice integrity means the interface buyers see supports comparison rather than obscuring it, a point that becomes central in digital markets, because design and defaults shape effective demand. (OECD)

Falsifiers are essential because they keep you honest. If you observe durable price dispersion that aligns with cost differences, vigorous entry that scales, and clear pass-through where lower fees translate into lower prices, the “hidden market power” story becomes weaker. If you observe stable access after off-channel discounts, and sellers routinely steer customers to cheaper routes without losing visibility, your market looks closer to the competitive benchmark.

Key terms

- Perfect competition, a benchmark model with free entry and price-taking behavior (OpenStax)

- Long-run equilibrium, the state where entry and exit stop because economic profit is zero (OpenStax)

- Pass-through, how much a cost or fee change shows up in consumer prices

- Contestability, the ease with which entrants can challenge incumbents

Choice integrity, the extent to which buyers can meaningfully compare offers - Substitution, the ability of buyers to switch, the engine behind price discipline

WHY PLATFORMS CHANGE THE GAME

A platform is a market that also owns the map. You do not walk past shops the way you do on a real street, you get routed, sorted, filtered, and nudged. The map decides what you notice, and what you never see.

When the map becomes the default, people stop asking “who is cheapest,” they ask “who is safest,” and safety gets defined by a button, a badge, a rank, and a familiar checkout flow. Sellers learn that their real competition is no longer the shop next door, their real competition is invisibility.

That is how you get a strange modern mood, the market looks full, lots of sellers, lots of products, endless scroll, yet prices feel sticky and entry feels theatrical. The fight moves away from value and toward access. If you want to talk about competition today, you have to talk about the map.

Example

Two sellers offer the same product at the same price. One is “default,” one is “other options.” Most people buy from the default seller without thinking, because life is busy and trust is scarce. The non-default seller does not lose because of price or quality, he loses because of placement, and he starts spending money or changing behavior to get placement back.

What to watch for

- One interface becomes the “front door” for discovery, and rivals struggle to get attention

- Defaults and badges decide outcomes, even when many sellers exist

- Sellers spend more on visibility and compliance than on lowering prices

- Switching is possible, yet feels annoying enough that people rarely do it

- Rules feel vague, enforcement feels unpredictable, sellers behave carefully

- Competition shifts toward access, advertising, and bundled services

🔽 Click to Expand: The Economics

Platforms are often two-sided markets, they match buyers and sellers and set rules that manage trust, search, and transaction friction. In many digital markets, network effects and scale economies in data, reputation, and logistics can make a single interface disproportionately important as the point of discovery. (OECD)

This creates gatekeeper power through a bundle of control points, ranking, defaults, eligibility criteria, identity and reputation systems, and enforcement. The economic move is subtle, control of the funnel lets a platform affect the payoff to competitive behavior. If a seller fears losing default placement or visibility, the seller may avoid off-platform discounts, avoid multi-homing strategies, buy more complements, or reshape products to satisfy opaque criteria. None of this requires an explicit rule that says “you may not compete.” It works through expected loss and risk management.

Competition policy discussions across jurisdictions regularly highlight recurring conduct patterns that matter in platform settings, self-preferencing, tying and bundling of complements, restrictions that increase switching costs, and other forms of conduct that can degrade contestability even when nominal entry remains high. (OECD)

A useful way to keep the analysis grounded is to separate efficiency from exclusion. Efficiency shows up as lower search costs, less fraud, faster fulfillment, clearer product information, and better matching. Exclusion shows up when the same tools systematically raise rivals’ costs, block fee competition from passing through to consumers, or make switching and multi-homing unattractive. Evidence you can look for includes default sensitivity, ad intensity trends, multi-homing rates, and the degree to which interface design shapes consumer choices, a theme the UK CMA explores through online choice architecture and its potential harms to competition and consumers. (GOV.UK)

Key terms

- Two-sided market, a platform serving two groups where each side’s participation affects the other (OECD)

- Network effects, value rises as more users join, often reinforcing concentration (OECD)

- Gatekeeper power, control of access to demand through ranking, defaults, and rules (OECD)

- Defaults, design choices that steer most demand to one option

Multi-homing, using multiple platforms, crucial for keeping markets contestable - Online choice architecture, interface design that shapes decisions and can harm competition (GOV.UK)

PART II — THE PATTERN BOOK

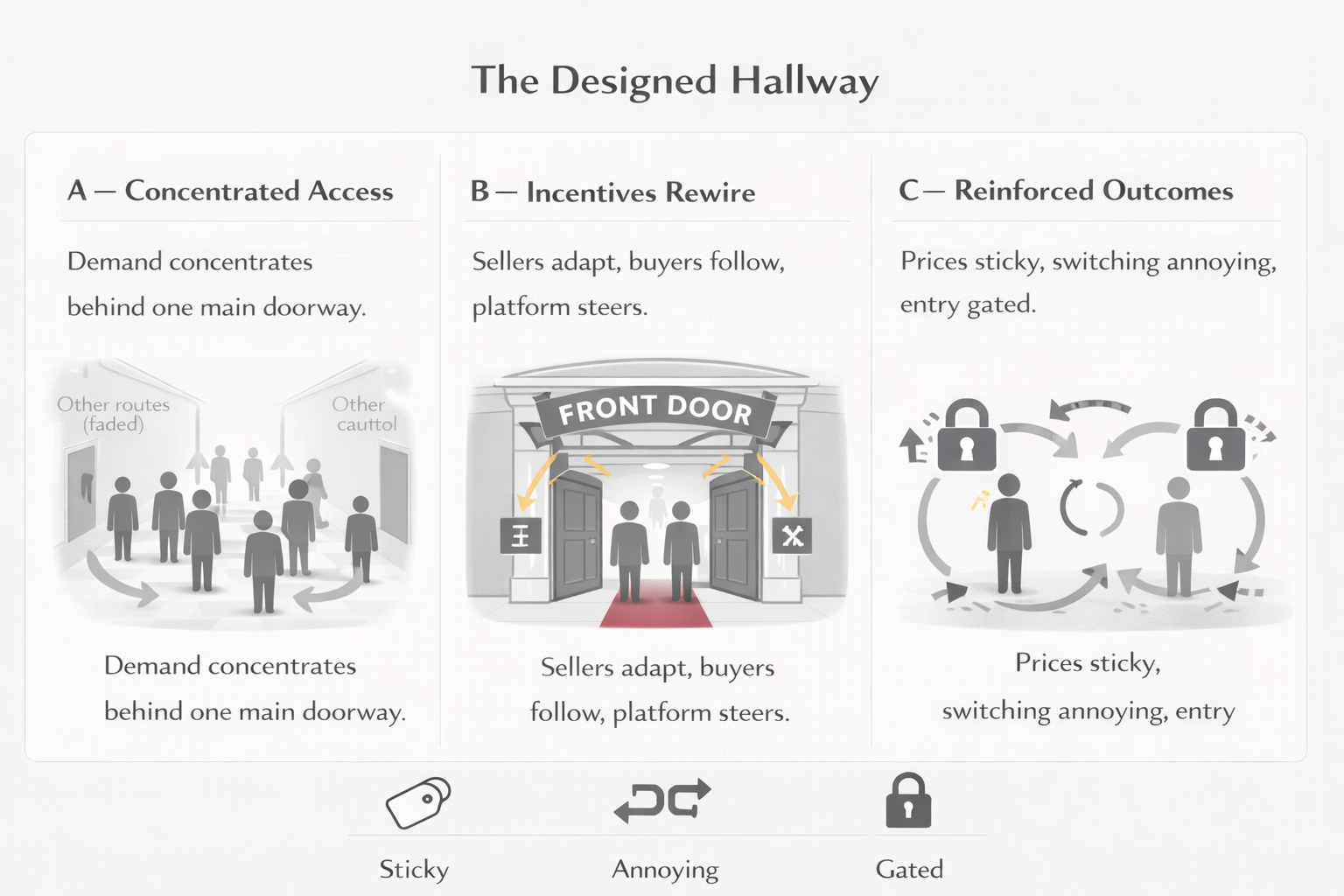

Now that we have a simple definition of competition, pressure on price and quality, easy switching, credible entry, we can look at the repeatable ways that pressure gets softened in modern platform markets. The patterns below are refer to incentives playing out in predictable ways once one doorway becomes more important than the rest. A seller who depends on a single demand funnel becomes cautious, a buyer who is busy follows defaults, a platform that controls the map can steer outcomes without shouting.

The same market can show several patterns at once, and the patterns often reinforce each other. A hidden price floor becomes stronger when sellers cannot steer customers, pay-to-play shelves become stronger when defaults dominate, switching friction makes everything stickier, and sticky markets are the ones where prices and fees stay confident.

Example

A consumer wonders why prices look similar everywhere, and a seller says “that’s just the market.” Then you learn the seller avoids discounting on cheaper channels because it risks visibility, and you learn customers rarely switch because cancellation is annoying, and you learn most sales flow through one default button. Suddenly the “market” looks less like a free-for-all and more like a designed hallway.

What to watch for

- Patterns show up as outcomes first, sticky prices, weak pass-through, low switching, slow entry growth

- Sellers speak about eligibility and visibility, not only about rivals

- Buyers behave like humans, they follow defaults and avoid effort

- Rival channels fail to scale even when they offer lower fees

- Advertising looks like rent, not like optional marketing

- Rules feel discretionary, so firms self-censor

🔽 Click to Expand: The Economics

These patterns are a practical way to operationalize contestability, which is the central condition behind the “profit goes to zero” long-run competitive story. In the benchmark model, above-normal returns invite entry, entry expands supply, prices fall toward average cost, and economic profit is competed away, which is the mechanism behind the idea that long-run gains flow to consumers rather than staying as excess profit. (OpenStax, Entry and Exit in the Long Run)

Digital platforms often alter contestability through control points that sit upstream of price, ranking, defaults, governance, data access, interoperability, and multi-homing friction. Competition policy surveys treat these as recurring categories because they are portable across sectors, they apply to commerce, travel, app ecosystems, payments, food delivery, media distribution, and many other settings where discovery and trust are intermediated. (OECD, Competition Policy in Digital Markets)

The reason a “pattern book” helps is that many harms are not captured by counting sellers. A market can have many sellers and still be weakly competitive if attention is concentrated behind defaults, if switching is costly, if rivals cannot access demand efficiently, or if parity and anti-steering blunt price rivalry. A pattern lens also forces measurement, each pattern implies one or two core signals, and each pattern has falsifiers that would weaken the claim, which keeps the article honest and keeps it away from conspiracy thinking.

Key terms

- Contestability, entry and switching that constrain incumbents, the backbone of long-run competitive pressure (OpenStax, Entry and Exit in the Long Run)

- Bottleneck, control of a critical route to customers, often attention and defaults (OECD, Digital Markets survey)

- Reinforcement, patterns that amplify each other, parity plus anti-steering is a common pair

- Falsifier, evidence that would force a mechanism claim to weaken or change

- Choice architecture, interface design shaping what users choose, relevant for default power (UK CMA discussion paper)

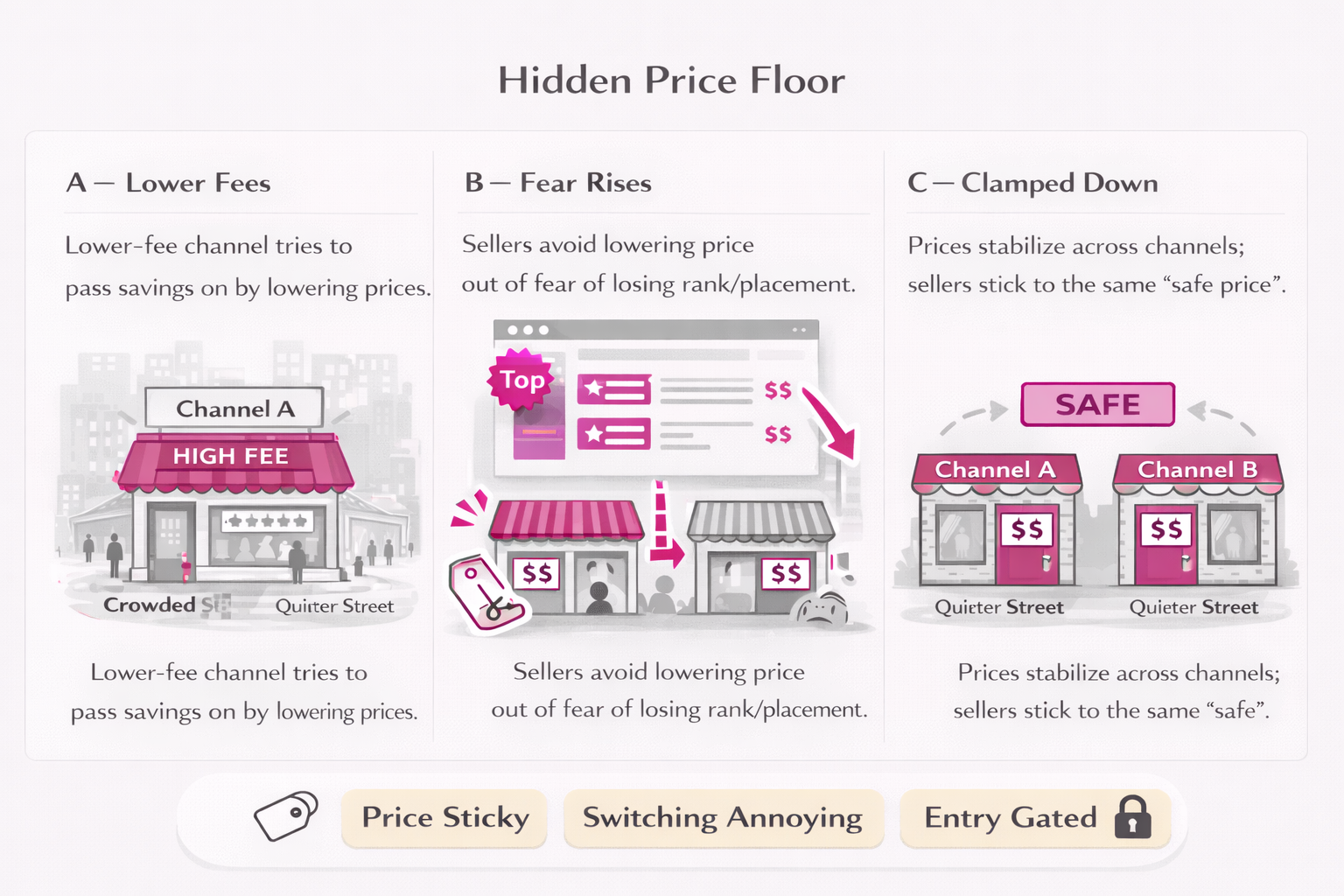

A healthy market rewards the person who finds a cheaper way to do business, because they can cut price and steal customers. A hidden price floor appears when that basic move becomes emotionally unsafe, sellers start thinking like nervous tenants, and the safest price becomes the same price everywhere.

You will hear people describe it as “keeping things consistent” or “protecting the brand,” yet the real force is usually fear of losing access to the biggest flow of customers. When one doorway matters far more than the rest, the seller’s first job becomes staying welcome at that doorway, and the easiest way to stay welcome is to avoid being “too cheap” somewhere else.

The result is oddly calm pricing, even in categories where you’d expect constant undercutting, because the market is busy on the surface and restrained underneath.

Example

A seller has two channels, Channel A is the crowded street with high fees, Channel B is the cheaper street with lower fees. The seller could cut prices on B, because lower fees give room to lower prices while keeping margin, yet the seller keeps prices aligned, because a small chance of losing visibility on A feels like a business-ending event.

So the cheaper channel never becomes meaningfully cheaper, rival channels never get the “growth oxygen” they need, and consumers never see the full benefit of lower costs.

What to watch for

- Prices for identical items cluster tightly across many channels, even when fees and operating costs differ materially

- Sellers talk about “staying competitive” in a way that sounds like staying eligible, not like winning customers through value

- Rival channels try lowering commissions, yet consumer prices stay sticky, the fee savings do not flow through to buyers

- Discounts exist, yet they appear small, temporary, or hidden behind awkward steps, rather than becoming a steady competitive weapon

- A seller’s biggest anxiety is losing placement, badges, or default access, and price decisions start revolving around that anxiety

- New entrants struggle to scale using a “low fee → lower price” strategy, because sellers won’t follow them with real price cuts

🔽 Click to Expand: The Economics

A “hidden price floor” is often produced by parity forces, sometimes written into contracts as most-favoured-nation clauses, sometimes achieved through softer commercial measures that punish sellers for offering better terms elsewhere. The economic point is simple: if a platform or intermediary can make sellers worse off when they discount on another channel, then sellers rationally avoid discounting, and the whole market looks like it has a price floor even though there is no explicit price control. (OECD)

Why this matters for competition is also simple: if a rival channel tries to compete by charging sellers lower fees, those fee savings should translate into lower consumer prices on that rival channel, because pass-through is one of the main ways competition benefits buyers. Parity restraints can block that pass-through, which means rival channels cannot win by being cheaper to sell on, and the dominant channel’s fee level becomes harder to challenge. This is the “raising rivals’ costs” logic in plain clothes, rivals can offer a better deal to sellers, and still fail to attract buyers, because sellers cannot safely price differently. (OECD)

Research on platform MFNs formalizes these effects and shows mechanisms through which parity clauses can raise platform fees and retail prices, and can discourage entry or distort entry strategies, especially for rivals trying to position as lower-cost, lower-price alternatives. (Chicago Unbound)

A practical measurement approach starts with three questions. First, does a seller discount elsewhere and then experience a measurable loss in visibility or conversion on the dominant channel, even when service quality remains constant. Second, do rival channels’ fee cuts fail to produce lower prices for consumers for identical products, which signals weak pass-through inconsistent with competitive pressure. Third, do you observe unusually tight price clustering for identical items across channels compared to what fee differences would predict. (OECD)

Falsifiers keep the story honest. If sellers routinely offer meaningfully lower prices on lower-fee channels without suffering visibility loss on the dominant channel, and if lower fees on rival channels produce persistent price differences that attract buyers and allow rivals to scale, then the “hidden price floor” story weakens substantially.

Key terms

- Parity clause / MFN, a rule that prevents sellers from offering better terms elsewhere, often framed as “most-favoured-nation” (OECD)

- Pass-through, the share of a cost or fee change that appears in consumer prices

- Raising rivals’ costs, conduct that prevents rivals from winning through lower costs or lower fees (OECD)

- Price clustering, unusually tight price similarity across channels for identical items, beyond what costs predict

- Contestability, whether entrants can scale enough to constrain incumbents

- Soft retaliation, changes in ranking, eligibility, or default placement that change seller incentives without explicit bans (OECD)

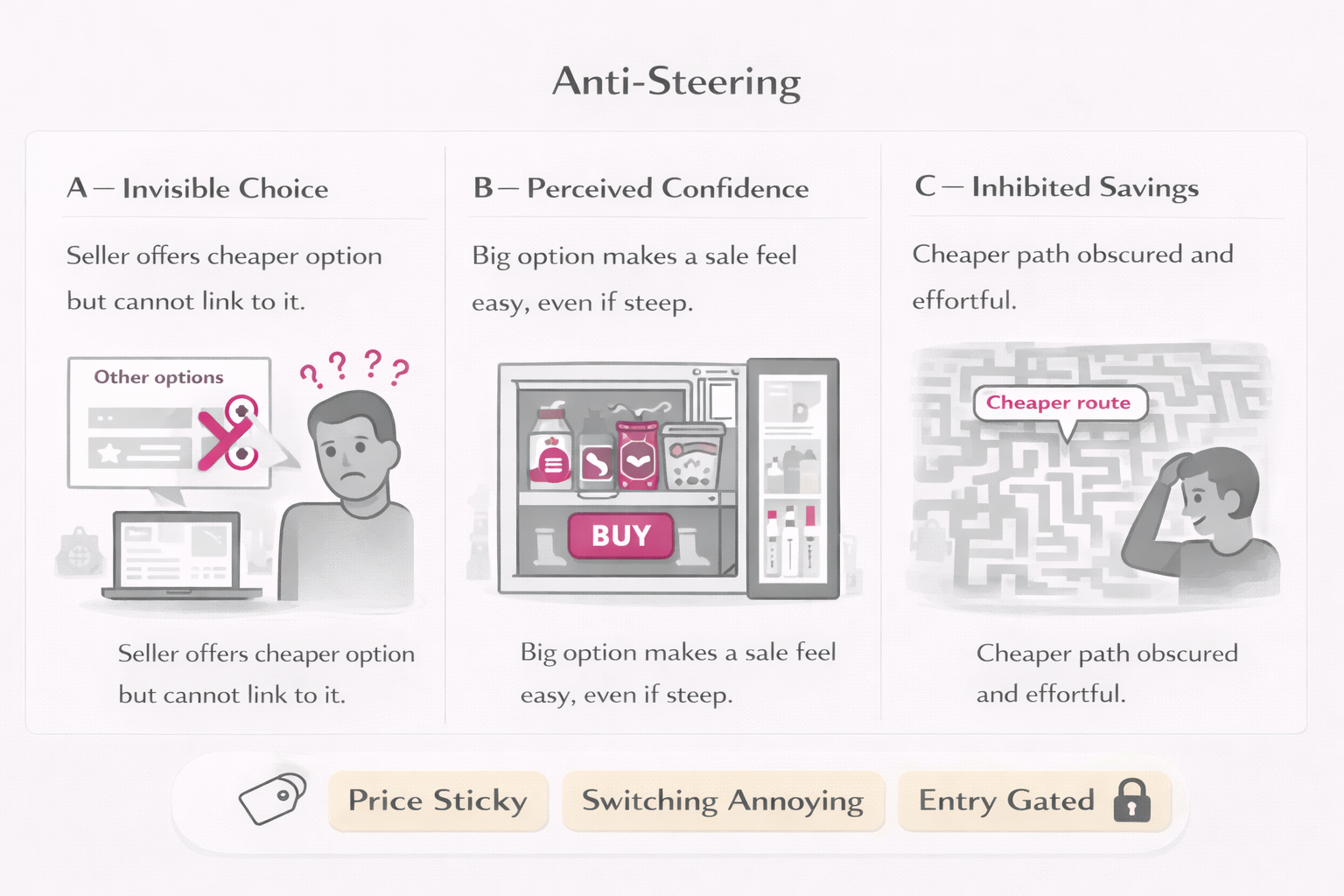

A free market works when the customer can find the better deal, and the seller is allowed to say, very calmly, “If you buy it this way, it’s cheaper.” Anti-steering is the opposite vibe, the seller can offer a cheaper route, yet the seller cannot mention it, link to it, or make it easy.

When that happens, the market starts feeling like a hotel minibar, everything looks available, and the prices look strangely confident. Customers cannot compare without effort, and most people don’t do effort, they do convenience, especially when they are tired or busy.

So the competitive weapon that should be most powerful, better pricing through a cheaper channel, loses power, because it is gagged at the moment where it would matter.

Example

A customer is about to pay, the seller knows there is a cheaper option, the seller is willing to offer it, and the customer would gladly take it. Yet the seller’s interface, rules, or contract says the seller cannot direct the customer there, cannot send a message, cannot show a link, cannot even hint too clearly.

The customer pays more, not because the cheaper option doesn’t exist, but because the market makes the cheaper option socially hard to reach.

What to watch for

- Sellers avoid mentioning alternative buying routes even when customers ask, the silence feels practiced

- Links out to alternative checkout options are blocked, discouraged, or buried in places most humans never see

- Discounts appear off-channel, yet customers inside the dominant channel never learn about them

- Rival channels struggle to grow because consumers never get routed to them, even when they offer better terms

- Sellers describe fear around “communication,” not only around price

- Price comparison becomes a hobby, not a normal consumer habit, because the interface makes it cumbersome

🔽 Click to Expand: The Economics

Anti-steering rules restrict how business users communicate and route consumers to alternative channels, which directly increases consumer search costs. The economics is straightforward: when search costs rise, fewer buyers compare, demand becomes less price-elastic, and sellers face weaker pressure to lower prices, which can increase markups and soften competition even in markets with many sellers. (OECD)

In digital markets policy discussions, anti-steering is frequently grouped with parity clauses because both mechanisms can protect a dominant intermediary’s position by limiting rivals’ ability to compete on price and by preventing sellers from passing on lower fees through lower prices on alternative channels. Anti-steering can therefore operate as a complement to the hidden price floor, parity blocks price differences, anti-steering blocks the communication of price differences, and the combination can be particularly effective in keeping competitive pressure muted. (OECD)

The key economic harm is not moral, it is mechanical. A rival channel can offer sellers a lower take rate, sellers can offer consumers lower prices, yet consumers do not learn about it at the decision moment, because steering is restricted. That blocks the “routing” function of competition, the ability for demand to flow toward the better deal, which is one of the main ways markets discipline prices. (OECD)

How to measure this without vibes: look for systematic gaps between the existence of cheaper offers off-channel and the visibility of those offers to consumers who start their journey on the dominant channel. Measure the friction, clicks required to discover alternatives, the ability to include links, the ability to message customers, and the degree to which customer retention is artificially tied to the original channel. Pair that with price effects, categories with stronger anti-steering should show weaker price competition and higher effective markups, all else equal. (GOV.UK)

Falsifiers matter here too. If sellers can freely communicate alternative prices and routes, and if consumers routinely learn about and use cheaper channels, then anti-steering is not binding in practice, and it cannot be doing much competitive work.

Key terms

- Anti-steering, restrictions that prevent sellers from directing consumers to alternative channels (OECD)

- Search costs, the time and effort required for consumers to compare offers

- Price elasticity of demand, how much demand responds to price changes, a key driver of price discipline

- Routing, the flow of demand toward better deals, which keeps markets honest

- Markups, the wedge between price and cost, which can rise when comparison is harder

- Friction, measurable steps, time, or obstacles required to reach an alternative route (GOV.UK)

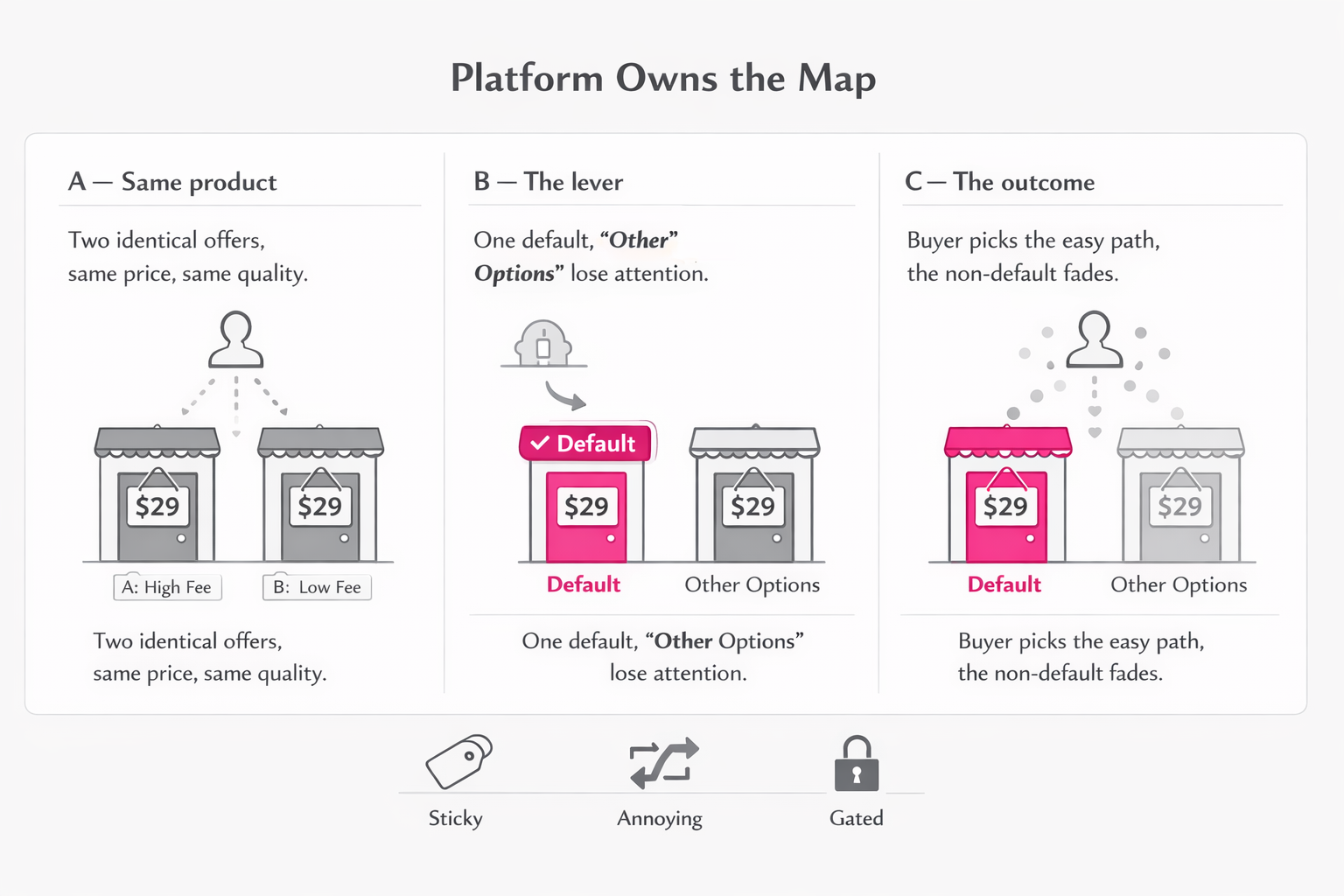

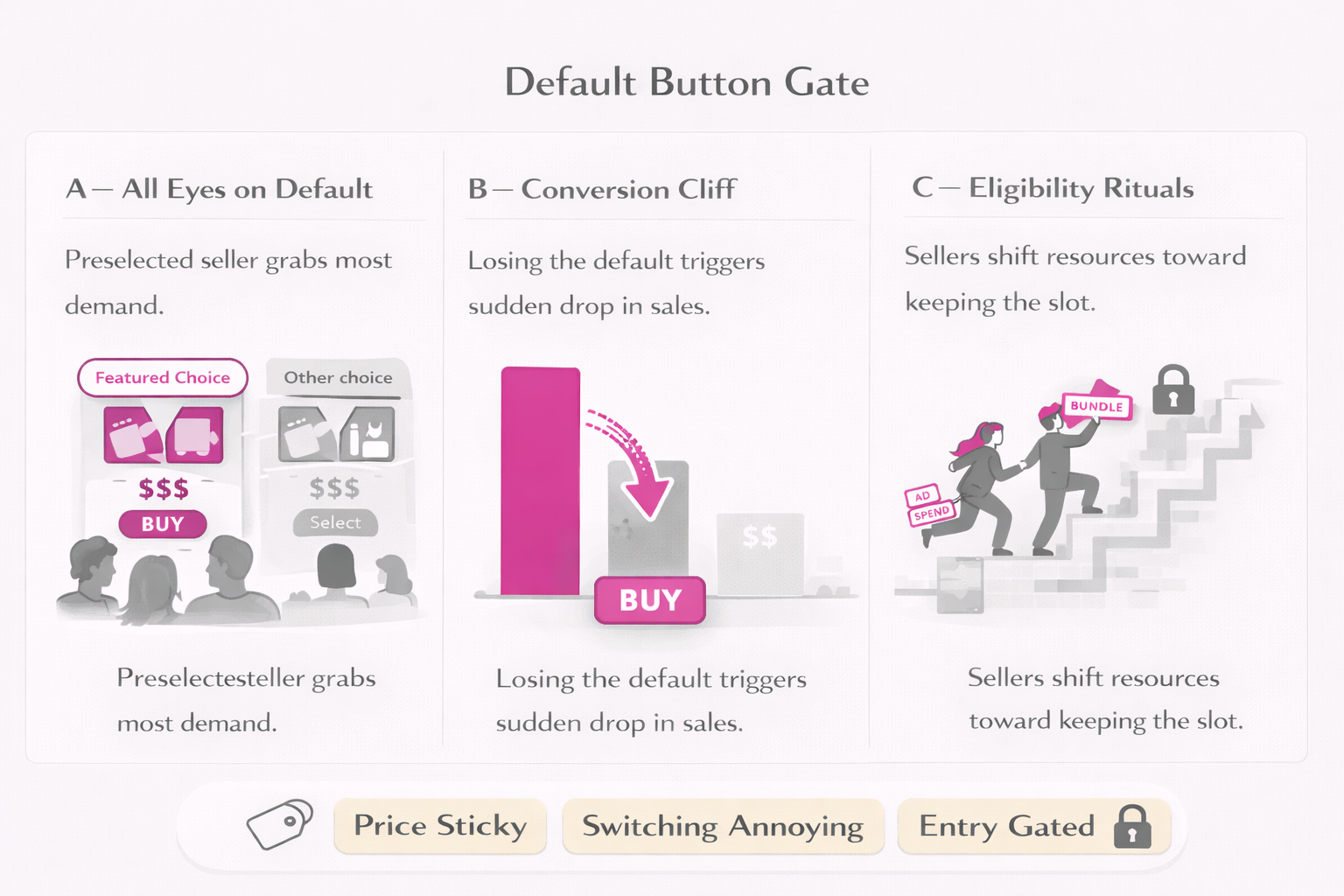

Most people choose the option that looks safest, fastest, and least likely to waste their time. A default button, a preselected option, a featured choice, these are small design choices that become huge economic forces when the platform becomes the main doorway to the market.

When the default becomes powerful, sellers stop asking “How do I beat my competitor on price,” and they start asking “How do I stay the default.” That shift matters because it changes what businesses invest in, instead of lowering prices or improving quality, they invest in eligibility rituals, paid visibility, and rule compliance that keeps them from falling out of the default slot.

The market still looks busy, yet competition starts to feel like theatre, because the default quietly decides who lives.

Example

Two sellers offer the same product at similar quality and similar total price. One is shown as the preselected option, the other is an “other choice.” The preselected seller gets most of the sales, not because the deal is dramatically better, but because buyers are human and time is scarce.

The non-default seller learns a harsh lesson, price cuts may not matter if they don’t change default status, so the non-default seller shifts budget away from price and toward whatever improves their odds of becoming the default.

What to watch for

- A single preselected option captures most demand, and other options feel like a hidden menu

- Losing default placement causes a sudden sales cliff, even when price and service do not change much

- Sellers talk about “winning the slot” more than “winning the customer,” and the language sounds like compliance

- Advertising spend rises because it is the only way to appear near the default

- Small rule changes or scoring tweaks cause big reallocations of seller behavior and budget

- Buyers stick with the default because the interface frames it as the safe choice, and the effort of comparing feels irrational

🔽 Click to Expand: The Economics

Defaults are powerful because humans exhibit inertia, limited attention, and a tendency to treat the default as advice. Classic evidence shows defaults can dramatically change decisions even in high-stakes contexts, because opting out requires attention and effort, and many people accept the default even when they have preferences. (Dan Goldstein)

In market design terms, this means the platform’s choice architecture can shape demand without changing the underlying set of sellers. When the platform is the main discovery route, controlling the default is close to controlling the market outcome, because the default captures disproportionate conversion. That creates a new competitive target, sellers compete for default eligibility and positioning, and this can redirect competition away from price and quality toward whatever the platform rewards, which may include paid visibility, bundled complements, or compliance with opaque rules. (GOV.UK)

This is where competition analysis shifts from counting the number of sellers to understanding the distribution of attention. A market can have thousands of sellers, and still behave like a concentrated market if attention is funneled to one default option. The relevant question becomes, how contestable is the default, how transparent are the criteria, and how much can rivals overcome default disadvantage through better value. (GOV.UK)

Measurement is concrete. Estimate the conversion difference between default and non-default positions for comparable offers, then analyze event-style shocks where a seller loses or gains default status. If sales move dramatically without corresponding changes in price or service quality, default power is doing heavy lifting. Combine that with indicators of seller behavior, rising “eligibility spend,” higher ad intensity, and strategic bundling to meet default criteria. (GOV.UK)

Falsifiers again keep discipline. If buyers routinely compare and frequently choose non-default options when they offer better value, and if sellers can gain share through price and quality improvements without needing default status, then the default is less of a gate and more of a helpful suggestion.

Key terms

- Default effect, the tendency for outcomes to follow the preselected option, often strongly (Dan Goldstein)

- Inertia, people stick with the current or suggested option because changing requires effort (NBER

- Choice architecture, how options are presented, which shapes decisions (GOV.UK)

- Attention funnel, the distribution of consumer attention across options, often highly skewed

- Contestability of defaults, whether better value can reliably win visibility and conversion

- Conversion cliff, abrupt sales change when a seller loses a key placement position

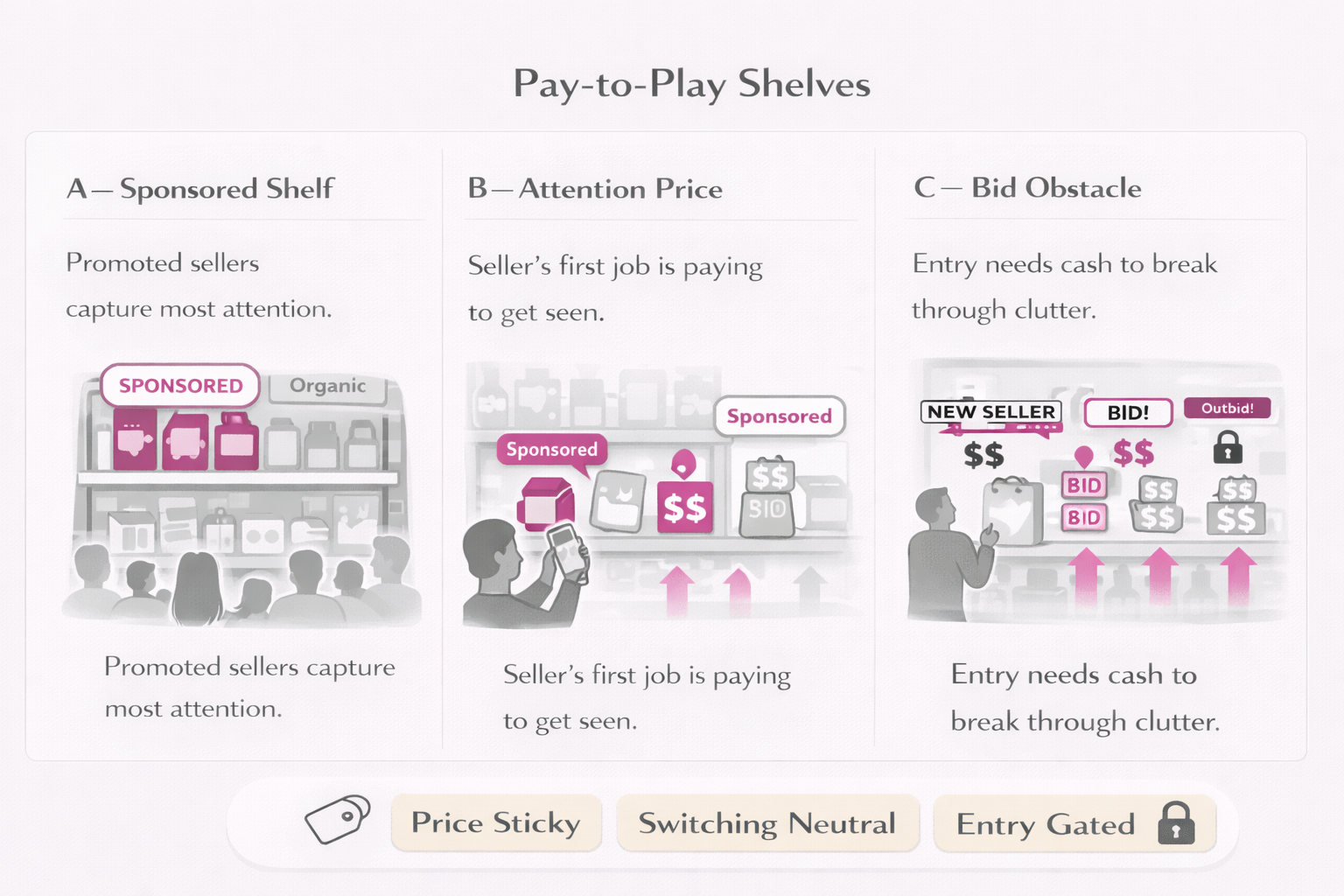

A store shelf looks neutral, a place where the best product wins because customers can see it and choose it. A pay-to-play shelf is a different creature, shelf space becomes rented space, and the rent is paid in advertising, promoted placement, sponsored visibility, and little fees that feel optional until you try to live without them.

This changes the way the market disciplines greed. In a normal free market, a seller who cuts costs can cut prices and gain share. In a pay-to-play market, the seller who cuts prices often discovers a second bill waiting in the shadows, “visibility rent,” and the market starts treating discovery like a toll road.

Over time, you see a quiet shift. Sellers don’t talk about beating rivals with better value, they talk about maintaining traffic, maintaining rank, maintaining impressions, maintaining eligibility to be seen. The consumer still sees a crowded shelf, yet the shelf behaves like a leased billboard, and the cost of the billboard flows into the final price one way or another.

Example

A new entrant offers the same quality at a lower price because they operate leaner, and this should be the classic free-market story. The entrant shows up on the shelf, then realizes the shelf is not where the customer looks, the customer looks where the platform points.

So the entrant pays to be pointed at, and the cost of being pointed at grows, because everyone else is paying too. The entrant’s “low cost advantage” shrinks, the price cut becomes smaller, and the consumer sees less benefit than the economics textbook promised.

What to watch for

- Sponsored placements grow until they feel like the main shelf, and organic discovery feels like a back room

- Sellers’ ad spending rises as a share of revenue even when their product and service stay stable

- The cost of staying visible rises faster than the cost of improving the product

- Entry becomes expensive on day one, because “paying for attention” becomes mandatory in practice

- Price cuts become less powerful than ad budgets, because visibility dominates conversion

- Sellers describe a treadmill effect, spending more just to stand still, rather than spending to grow

🔽 Click to Expand: The Economics

Pay-to-play shelves are best understood as a reallocation of competition from “price and quality” toward “purchased attention.” In many digital markets, advertising is not merely a marketing choice, it becomes an access price, because the platform controls discovery, ranking, and the path that buyers follow. When a large share of demand is funneled through a small number of interfaces, the platform can effectively auction a critical input, attention, and firms pay because the alternative is invisibility. The UK Competition and Markets Authority describes how market power in online platforms and digital advertising can arise through scale, access to data, and bottlenecks in user attention, and how a lack of transparency and conflicts of interest in ad systems can undermine competition. (CMA market study final report, 2020)

The OECD’s work on digital advertising markets explains why auctions and ad-tech intermediation matter, and why auction rules, market concentration, and conflicts of interest can affect outcomes when competition is weak. This matters to the “pay-to-play shelf” story because sellers end up paying through the chain to reach buyers, and those costs can act like an implicit tax on participation, particularly for entrants who lack brand recognition and must buy attention. (OECD, Competition in Digital Advertising Markets)

A simple economic diagnosis uses three steps. First, measure “visibility dependence,” the share of sales attributable to paid placements versus organic discovery, and how that share changes over time. Second, measure “ad intensity,” ad spend as a share of revenue, and test whether it rises even when product quality and prices are stable, which suggests rent extraction rather than growth investment. Third, test “contestable entry,” can a new seller gain share through lower prices and better quality without immediately buying attention at scale, or does entry require ad spend that erases the cost advantage. This is closely connected to the broader competition policy concern that markets can look crowded while remaining hard to contest, because control of attention can act like a gate. (OECD, Competition Policy in Digital Markets, 2024)

Empirical work on marketplaces also treats advertising as a strategic dimension of seller competition alongside pricing, which reinforces the point that paid visibility can become a central competitive lever rather than a peripheral one. (Shen, “Price and advertising competition in an online marketplace,” 2023)

Falsifiers matter because advertising can be legitimate. The pay-to-play harm story weakens when high-quality entrants can win meaningful organic discovery, when ad intensity stays stable as markets mature, and when paid placement remains clearly labeled and does not displace the consumer’s ability to compare value across a meaningful set of options.

Key terms

- Visibility rent, spending required to stay seen, beyond what is needed for normal marketing

- Ad intensity, advertising spend as a share of seller revenue, useful as a “treadmill” indicator

- Auctioned discovery, ranking and placement allocated through bidding rather than merit alone (OECD digital ads report)

- Contestable entry, ability for entrants to scale through value rather than paywalls (OECD digital markets report)

- Attention bottleneck, concentration of user discovery in one interface, enabling rent extraction (CMA final report)

- Displacement, paid placements crowding out organic comparison opportunities

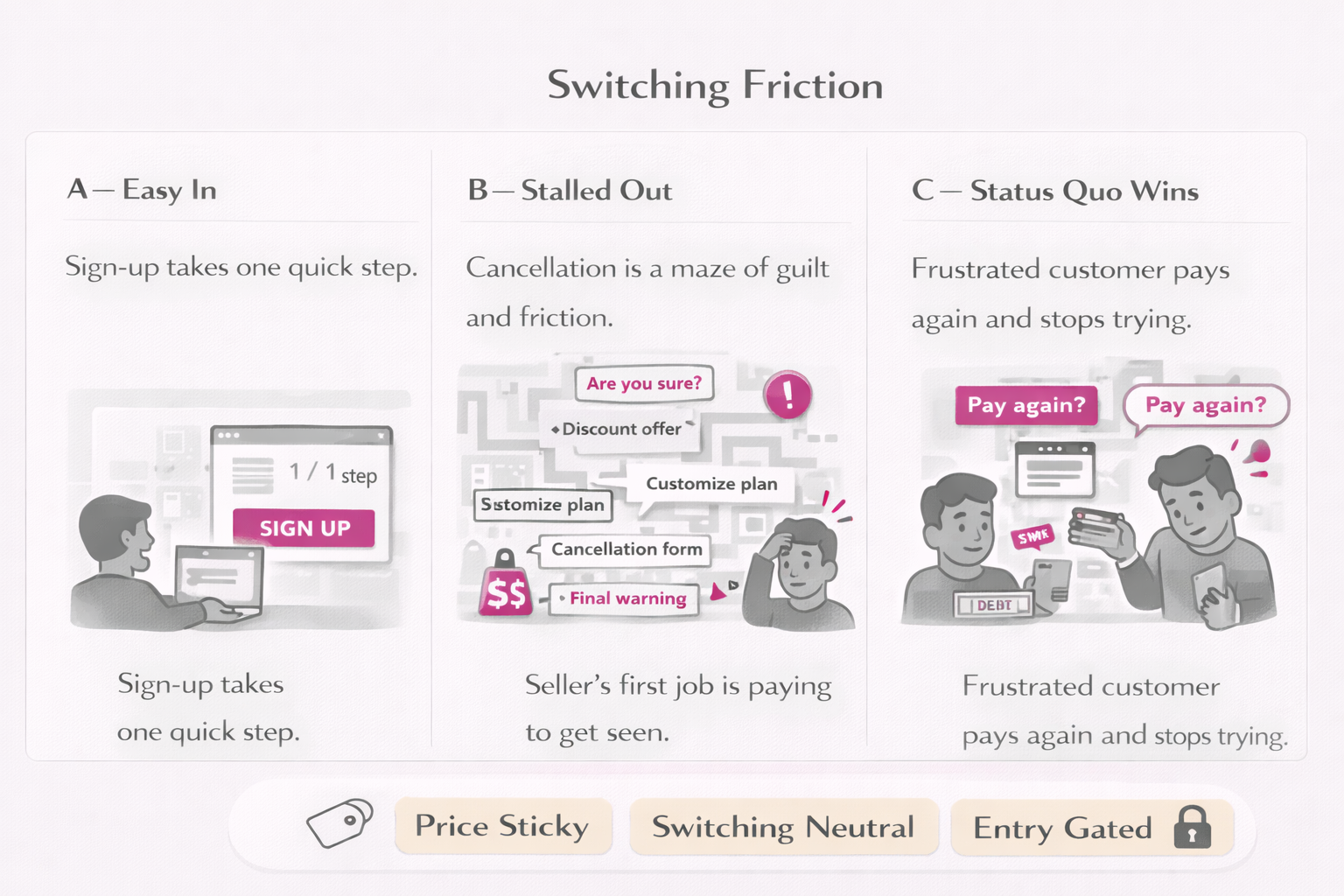

Leaving a store should feel like walking out the door. In many digital markets, leaving feels like a small administrative project, and that feeling is the whole point. When switching is annoying, people stay. When people stay, sellers have less fear. When sellers have less fear, prices and quality stop being disciplined the way free markets promise.

This pattern rarely shows up as a villain twirling a mustache. It shows up as friction, extra clicks, confusing wording, guilt-flavored popups, hidden settings, “are you sure” screens, cancellation steps that feel like a maze, and small obstacles that add up to a large behavioral wall.

A market can remain technically open, you can leave, you can compare, you can choose something else. The market still becomes sticky because most humans conserve attention, and the sticky option wins by exhausting the customer into acceptance.

Example

A person signs up in thirty seconds. They try to cancel later and discover five screens, three warnings, and a strange set of options that sound like they are designed to make cancellation feel like a mistake.

Many people quit the cancellation attempt halfway, then forget, then pay again, then stop caring because life is busy. The firm keeps revenue. The rival loses a chance to win a customer. The market’s “pressure” gets softer without anyone raising their voice.

What to watch for

- Joining is quick, leaving is slow, and the difference feels deliberate

- Cancellation is buried under vague menus or confusing language

- The interface uses urgency, guilt, or confusing defaults to keep users from switching

- Customers routinely pay longer than intended, then blame themselves

- Firms compete on “retention design” more than on lower prices

- Complaints cluster around cancellation difficulty, hidden charges, and accidental renewals

🔽 Click to Expand: The Economics

Switching costs create market power by limiting consumers’ ability to change suppliers, and that reduces the competitive constraint on price and quality. This is a classic result in industrial organization, and it applies strongly in digital settings because switching costs can be engineered through user interface design, account portability limits, and cancellation friction. A clear statement of the general idea appears in research that models search costs and switching costs together and shows how these frictions constrain competition and affect welfare. (Wilson, “Market frictions: search costs and switching costs,” 2012)

Regulators now treat “harmful design” as an economic issue, not only a consumer-protection issue, because design can suppress comparison and reduce switching, and those behaviors affect competitive outcomes. The UK CMA’s work on online choice architecture discusses how digital design practices can distort consumer choices and harm competition and consumers, including practices that make cancellation difficult or that steer users toward outcomes that benefit the firm. (CMA Online Choice Architecture discussion paper)

The OECD has also documented “dark commercial patterns” and the evidence on their prevalence and harms, including patterns that make cancellation hard or that push consumers into unwanted purchases, and it frames these practices as a systematic feature of online business models rather than isolated misbehavior. (OECD, Dark Commercial Patterns)

From a measurement perspective, this pattern is unusually testable. You can build a “switching friction index” from steps, time, and error rates required to cancel, downgrade, delete, export data, or move accounts. You can compare that friction to the ease of sign-up, and you can track how changes in friction correlate with churn, pricing, and complaint rates. You can also test whether markets with higher friction show weaker price sensitivity and higher markups, consistent with theory.

Falsifiers strengthen the credibility of your analysis. The switching-cost harm story weakens when cancellation and portability are genuinely symmetrical with sign-up, when consumers switch frequently, and when firms with worse prices lose share quickly because customers can leave without effort.

Key terms

- Switching costs, time, effort, and loss involved in moving to a rival, creating “stickiness” (Wilson 2012)

- Online choice architecture, design choices that shape decisions and can harm competition (CMA OCA paper)

- Dark patterns / dark commercial patterns, interface tactics that steer users toward firm-beneficial outcomes (OECD report)

- Friction asymmetry, easy entry and difficult exit, a common competitive lever

- Churn, the rate at which customers leave, a key outcome variable

- Sludge, burdens that reduce take-up of beneficial actions, related to transaction costs (overview: Behavioural Public Policy, 2024)

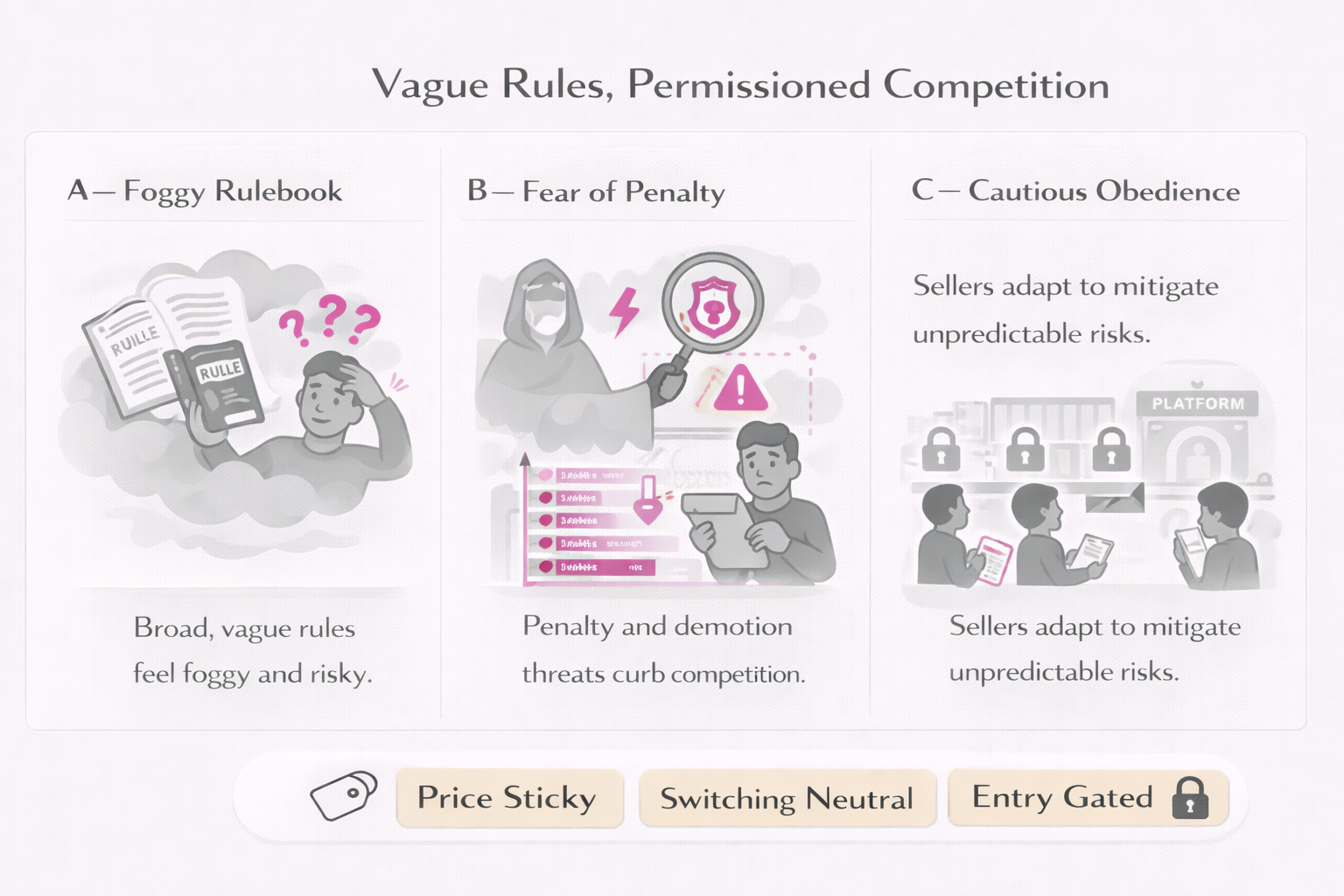

A normal market has rules that feel boring. You pay, you deliver, you treat people decently, you compete, you win or lose. A permissioned market has rules that feel foggy, and the fog becomes a form of control.

The seller learns a new kind of discipline. The seller asks, “Will this strategy upset the gatekeeper.” The seller avoids anything that might trigger a penalty, a demotion, a suspension, a loss of a badge, a loss of default placement, a loss of access to the customer. The seller becomes cautious in ways that look like “professionalism,” yet the caution drains the market of its sharp edge.

This pattern reduces competition without changing the number of sellers. Thousands of sellers can exist, and they can still behave like trained animals if the penalty risk is large and the criteria for punishment feel unclear.

Example

A seller considers a simple competitive move, lowering price on a cheaper channel, changing a return policy, offering a different shipping method, bundling a product differently, using a third-party tool to manage inventory. The seller can’t easily predict whether the gatekeeper’s scoring system will interpret the move as “bad behavior.”

So the seller does nothing. The seller stays inside the safe lane. The market stays stable. The consumer pays more for stability than they realize.

What to watch for

- Rulebooks that are long yet vague, filled with broad standards and discretionary language

- Enforcement that feels inconsistent across similar sellers or similar situations

- Appeals that feel opaque, slow, or unpredictable, so firms adapt by self-censoring

- Sellers describing “fear of the system” rather than “fear of competitors”

- Sudden policy changes that reshape categories or business models overnight

- Innovation that shifts from product improvement toward “compliance optimization”

🔽 Click to Expand: The Economics

Permissioned competition is governance as a competitive instrument. The mechanism is uncertainty combined with asymmetric dependence. When access to demand depends on compliance with criteria that are hard to predict, firms behave conservatively, and conservative behavior reduces rivalry. The expected-loss logic from the prologue applies again: a small probability of a severe penalty can rationally deter competitive actions even if those actions are economically efficient.

Competition policy work on digital markets consistently highlights concerns about opacity, lack of transparency, and conflicts of interest in platform governance, especially where platforms set the rules for others while participating in related markets or controlling critical access points. The CMA’s market study on online platforms and digital advertising includes discussion of how lack of transparency and conflicts can undermine competition, and it frames governance interventions as part of pro-competitive policy options. (CMA final report, 2020)

The OECD’s work on competition policy in digital markets similarly surveys conduct and enforcement concerns across jurisdictions, including practices linked to platform rule-setting, self-preferencing, and the use of data and access controls that can distort competition. This is relevant here because governance opacity amplifies all the other patterns: it makes sellers less willing to discount, less willing to multi-home, more willing to buy complements, and more dependent on paid visibility, because the safe strategy is the strategy that aligns with the gatekeeper’s incentives. (OECD, Competition Policy in Digital Markets, 2024)

Measurement can be grounded in observable events. Track enforcement actions, demotions, suspensions, badge losses, and reinstatements, and test whether these events are predictable from clear performance metrics or whether they are better explained by discretionary criteria. Look for “chilling effect” signals, sellers converging on similar safe behaviors, reduced experimentation, lower variance in pricing strategies, and rising spend on compliance and platform-preferred services.

Falsifiers are again useful. Permissioned competition is less of a concern when rules are specific, enforcement is consistent, appeal mechanisms are transparent and fast, and sellers can undertake aggressive competitive strategies without unexplained retaliation. In that world, governance supports trust and safety, and market pressure remains sharp.

Key terms

- Governance power, the ability to shape market outcomes through rules, enforcement, and discretion

- Chilling effect, competitive behavior that disappears because the risk of punishment is hard to price (OECD digital markets report)

- Opacity, lack of transparency in ranking, enforcement, or criteria, enabling discretion (CMA final report)

- Due process, predictable rules plus meaningful appeal, a competitive safeguard

- Dependency, the share of a seller’s business tied to a single gatekeeper, amplifying expected loss

- Compliance optimization, investment in meeting gatekeeper criteria rather than improving price and quality

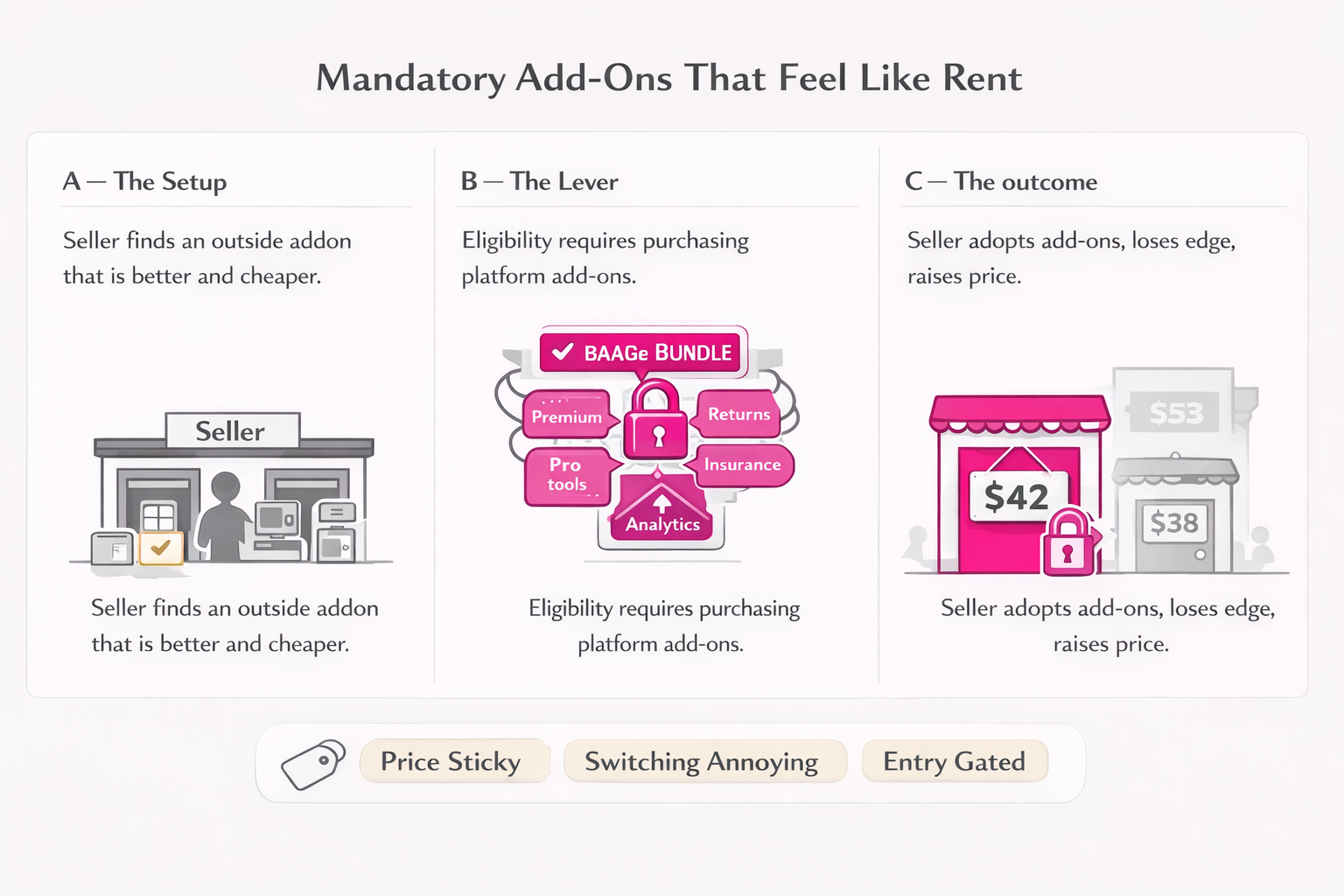

A normal market lets you run your shop like an adult. You pick the tools that fit your business, the cheapest payment option, the best shipping workflow, the simplest returns process, the marketing you can actually afford, and you compete by being better or cheaper. The tools compete for your business, and you keep the upside when you operate efficiently.

In some platform markets, the tools stop competing and start orbiting the gatekeeper. You can still “choose,” yet the choice feels ceremonial because the platform quietly treats certain add-ons as the price of being treated as credible. The seller learns an ugly truth: you are not only selling a product, you are selling inside a bundle, and the bundle includes complements, ads, “pro” analytics, premium customer support, verification programs, insurance, branded checkout, and other extras that sit next to the transaction like toll booths.

That is tying and bundling in everyday clothes. The bottleneck is not the add-on itself, the bottleneck is the doorway to demand, the default placement, the badge, the faster checkout, the eligibility to appear in the “top” filter. When those boosts are linked to the platform’s own complements, rival providers can be better and cheaper and still fail to win, because the competition stops being “best tool wins” and becomes “buy the right bundle or accept weaker access.” That is how foreclosure feels from the inside, you are not banned, you are just made less viable.

The consumer experiences it as smooth convenience, fewer scams, faster resolution, less mental load, and also pays for it through stacked tolls. A seller’s efficiency gains get absorbed by mandatory extras, so pass-through shrinks, prices stay confident, and competition shifts from “be cheaper” to “buy the bundle that keeps you visible.”

Example

A seller is doing fine until the platform introduces a “Trusted Seller” badge with a small boost in placement and conversion. The badge is framed as optional, a way to reassure buyers. Then the seller learns the practical requirements: enroll in the platform’s paid buyer-protection program, use the platform’s dispute-resolution workflow, accept a stricter returns policy, and subscribe to the platform’s “pro” messaging tools so you can respond within a required time window.

None of these add-ons is outrageous on its own. The problem is the bundle. Without the badge, the seller’s offer is shown lower, fewer buyers click, and the seller’s customer-acquisition cost rises because they have to buy more ads just to stay even. The seller does the math and realizes that “not buying the extras” is the expensive choice. So they pay for the badge bundle, raise prices a little to cover the new tolls, and the market loses a quiet source of price pressure, not because the seller became greedier, but because the doorway started charging rent in the form of complements.

What to watch for

- Sellers describe certain add-ons as “optional in theory, required in practice”

- Using outside tools seems to reduce conversion, visibility, or eligibility for key placements

- Sellers’ total costs become layered, listing fees, ads, logistics, payment, returns, analytics, all paid to the same gatekeeper

- Rival service providers struggle to compete even when they offer better price or quality

- Prices stay sticky because sellers spend their “efficiency gains” on tolls rather than passing them to buyers

- Competition shifts toward buying the right bundle instead of building the best offer

🔽 Click to Expand: The Economics

This pattern is the economics of tying and bundling applied to platform complements. A complement is any input that helps a seller reach customers or complete a transaction: payments, fulfillment, advertising, analytics, identity, dispute resolution, customer service tooling. When a platform controls discovery and conversion, it can influence the payoff to using complements, and it can do so in ways that reshape competition among those complements.

Tying means customers must buy one product to obtain another, and bundling means multiple products are offered together as a package. These strategies often generate efficiencies, smoother user experience, lower transaction costs, better trust and fraud control. They also create competitive risk when used to foreclose rivals, especially when the “tying product” is a bottleneck input such as access to demand, ranking visibility, or default placement. The OECD’s digital markets survey explicitly frames tying and bundling as conduct that can benefit consumers and can also harm competition when it excludes competitors from related markets. (OECD)

The crucial economic question is simple: do complements compete on merit, or does the platform make rival complements less viable by design or rule structure. Technical tying can appear through interoperability restrictions, and contractual tying can appear through eligibility conditions, both mechanisms show up repeatedly in competition discussions around digital gatekeepers. (OECD)

A grounded measurement approach looks at three outcomes. First, do sellers adopt the platform’s complements even when alternatives are cheaper, which suggests the complement purchase is driven by access rather than quality. Second, does the adoption correlate with gains in visibility or conversion unrelated to the intrinsic quality of the complement, which suggests a designed advantage rather than market competition. Third, do rivals in the complement market fail to scale despite competitive pricing, which suggests foreclosure rather than normal differentiation. (OECD)

Falsifiers keep the diagnosis honest. The “mandatory add-on” story weakens when sellers can use alternative complements without meaningful performance penalties, when ranking and defaults stay neutral to complement choice, and when rival complement providers can win share by offering better price and quality.

Key terms

- Tying, a requirement to purchase one product to get another, achieved technically or contractually (OECD)

- Bundling, selling multiple products as one package, sometimes efficient, sometimes exclusionary (OECD)

- Complement, an input that improves transaction completion, visibility, or trust

- Foreclosure, a rival’s inability to compete because access or interoperability is constrained (OECD)

- Bottleneck input, an asset that rivals need, such as access to demand or default placement

- Stacked tolls, multiple fees layered on the same seller journey, reducing pass-through to consumers

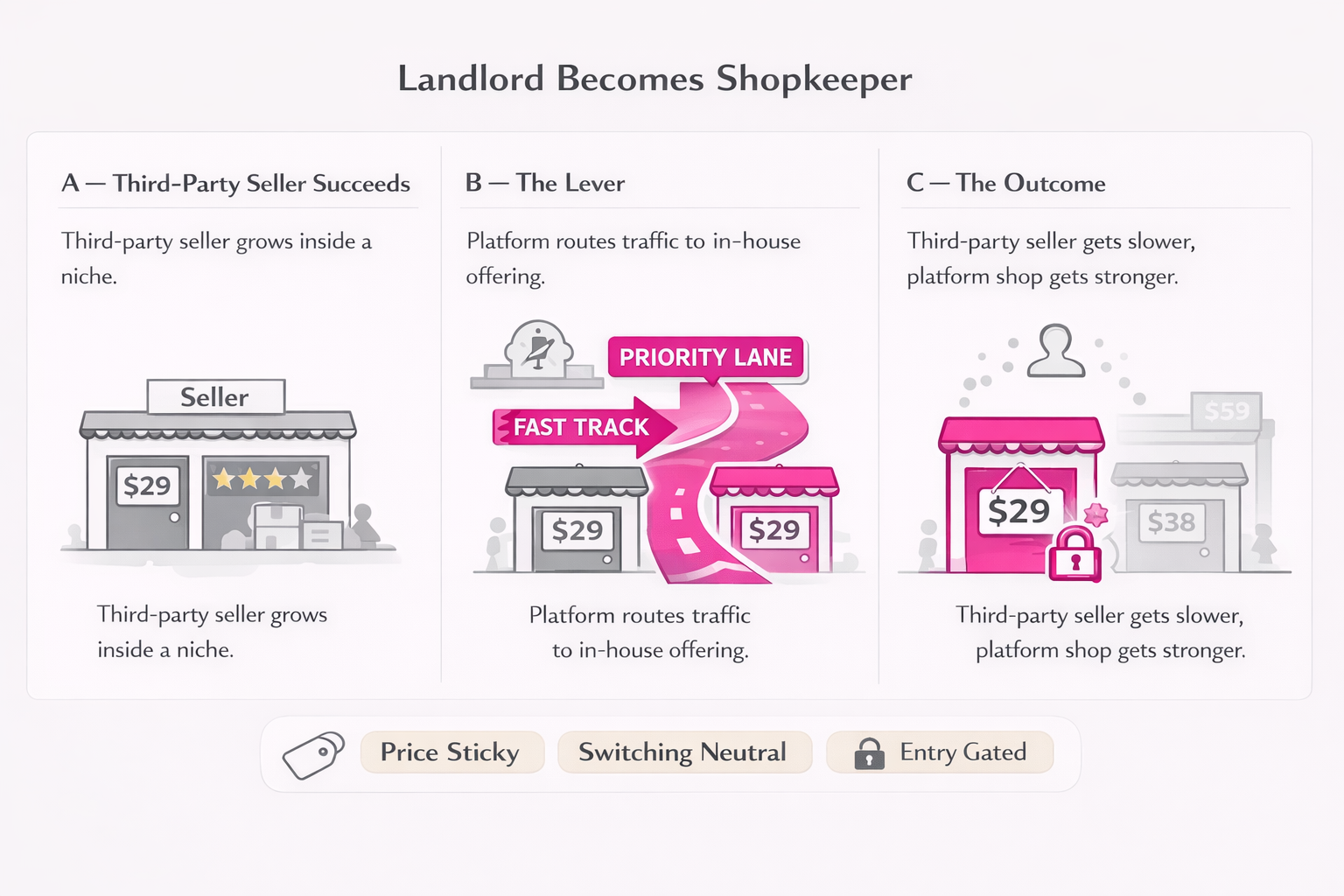

A market feels fair when the referee is not also playing striker. In a platform setting, the “landlord” often runs the mall and can also sell inside the mall, which creates a built-in temptation: the landlord controls the signs, the foot traffic, the recommended shelf, and the rules of the hallway.

When the landlord is also a shopkeeper, competition changes shape. Independent sellers stop seeing rivals as their main threat and start seeing the platform’s internal incentives as the main threat. The feeling becomes, “I can compete all day, yet I can still lose because the map decided I should.”

Consumers can still get convenience and sometimes good prices, and the market still risks losing the core free-market mechanism, the best deal winning because customers can reach it.

Example

A third-party seller succeeds in a narrow niche by refining quality, lowering returns, and improving service. The niche starts growing. Soon the platform introduces an in-house offering in the same niche, and the in-house offering benefits from prime placement and frictionless integration.

The third-party seller may not vanish, yet their growth slows sharply because the traffic that used to find them gets rerouted. The seller becomes less willing to invest in innovation because the expected payoff feels uncertain.

What to watch for

- The platform competes with sellers while also controlling ranking and default choices

- Placement advantages appear for the platform’s own offerings even when value looks comparable

- Rule enforcement feels stricter for third parties than for in-house offerings

- Sellers report “copy risk” and avoid investing in categories that look strategically interesting to the platform

- Category shifts occur soon after the platform launches a competing offering

- Sellers divert effort from product improvement toward survival tactics, ads, bundles, and compliance

🔽 Click to Expand: The Economics

This pattern is self-preferencing under vertical integration. It occurs when an intermediary controls the route to the customer and also competes downstream, creating incentives to tilt the route in its own favor. The competitive concern is not vertical integration itself; many integrated models are efficient. The concern is discriminatory treatment that changes contestability, rivals cannot win by being better because the funnel is tilted.

Economic analysis frames self-preferencing as a distortion of the competitive process, especially when the platform’s conduct results in exclusion of rivals or durable weakening of competitive constraints. Policy discussions on digital markets repeatedly treat self-preferencing as a central category because ranking, default placement, and recommendation systems are powerful allocation mechanisms for demand. (OECD)

The European Union’s Digital Markets Act explicitly targets discriminatory practices and equal treatment concerns in gatekeeper settings, which reflects the logic that contestable search and discovery requires protection against discriminatory routing by dominant intermediaries. (EUR-Lex)

A practical measurement approach focuses on controlled comparisons and event timing. Compare placement, conversion, and default status for platform-owned versus independent offerings controlling for price, delivery speed, return terms, ratings, and other quality signals. Then run event-style analysis around moments when the platform enters a category, changes ranking criteria, or modifies badges, and examine whether independent sellers’ visibility drops in ways not explained by value changes. (OECD)

Falsifiers matter. The self-preferencing story weakens when ranking criteria are transparent, consistently applied, auditable, and when independent sellers regularly win placement by offering better total value. It also weakens when the platform’s own offerings succeed primarily through genuine efficiency and price advantages that remain contestable by others.

Key terms

- Self-preferencing, preferential treatment of an integrated platform’s own offerings in ranking, defaults, or access (Bruegel)

- Vertical integration, a firm operating at multiple levels of the value chain, sometimes efficient, sometimes risky

- Discriminatory routing, steering demand toward preferred offerings through ranking or design (EUR-Lex)

- Conflict of interest, the platform’s incentives to favor itself while setting the rules

- Contestability, the ability of rivals to constrain an incumbent by offering better value (OECD)

- Auditability, the ability to test whether ranking and enforcement rules are applied consistently

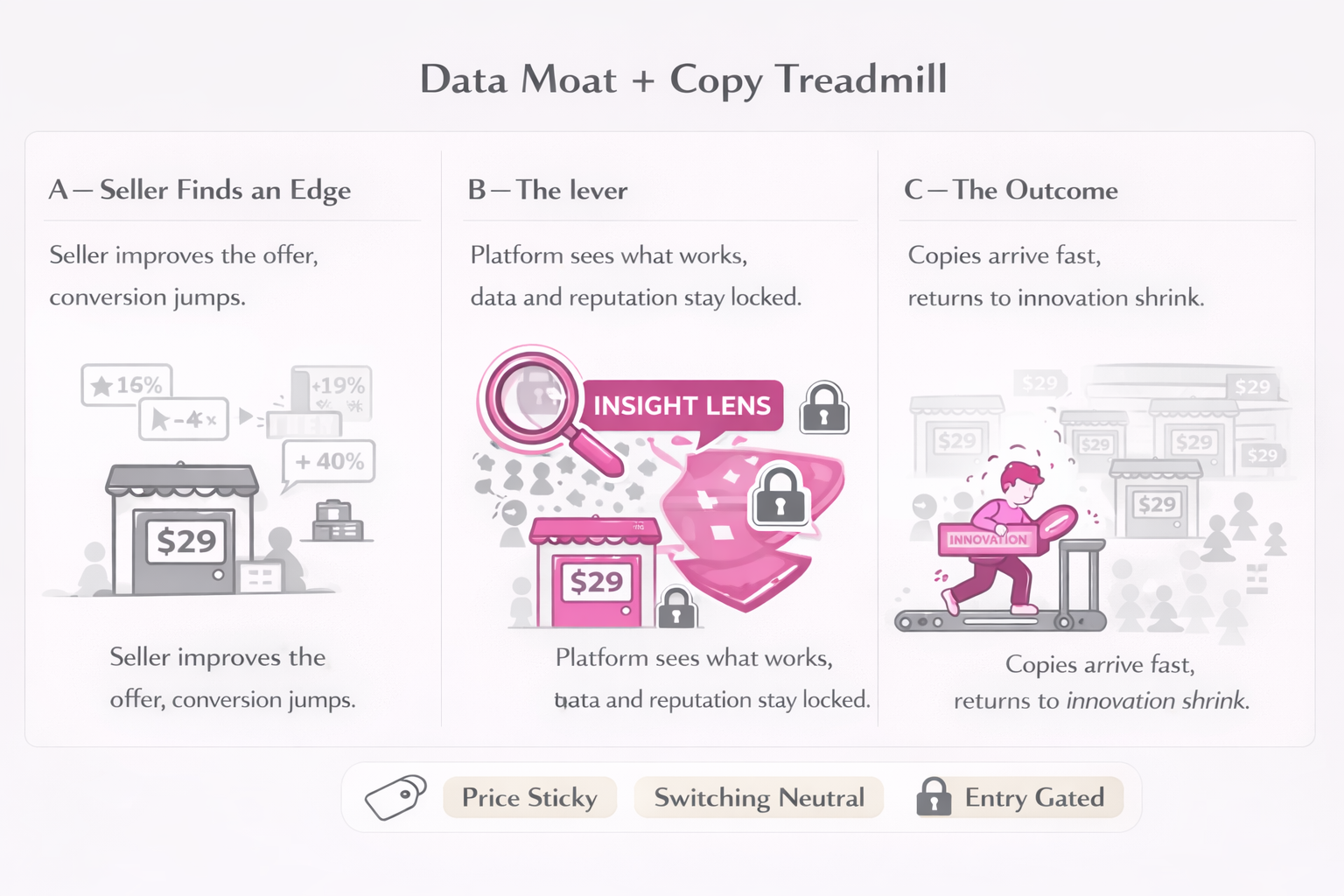

In a free market, innovation is supposed to be rewarded. You make something better, customers notice, you grow, and rivals respond by improving too. In some platform settings, success becomes unusually visible to the platform, and visibility changes the reward.

The seller’s fear becomes simple: “If I show what works, it will be learned instantly.” So the seller invests less, experiments less, and chooses safer, smaller bets. The market still produces products, yet it produces fewer bold improvements, because the treadmill speeds up and the finish line keeps moving.

The consumer still gets convenience, and the consumer also loses the long-run benefit of a market that rewards experimentation with durable returns.

Example

A seller discovers a better bundle, fewer returns, a clearer product description, a better packaging approach that reduces damage, a smarter pricing strategy. Sales climb. The platform can observe the entire funnel: search terms, conversion rates, refund rates, repurchase patterns, and price elasticity.

Soon the seller sees close substitutes appear and the category becomes crowded. The seller keeps operating, yet future investments feel riskier, because “being first” no longer yields a stable period of reward.

What to watch for

- Sellers describe shorter product lifecycles and weaker returns to innovation

- Successful niches become crowded unusually fast, especially around observable performance signals

- Sellers struggle to move reputation, reviews, or customer history to other channels

- Multi-homing is technically possible and practically hard because data stays trapped

- Entry thrives in low-observability categories and weakens in high-observability categories

- Innovation shifts from product leaps to small optimizations that avoid triggering imitation

🔽 Click to Expand: The Economics

Data moats operate through two channels: lock-in and learning advantage. Lock-in arises when users and business users cannot port their data, reputation, or workflow history, which raises switching costs and reduces the competitive threat from rivals. Learning advantage arises when the platform’s vantage point provides superior information about demand, pricing, and performance, which can accelerate imitation and reduce the private returns to innovation for dependent sellers.

The OECD has a dedicated analysis of how data portability and interoperability can promote competition by reducing consumer lock-in, enabling multi-homing, and supporting unbundling, while also noting that portability is not universally effective and can carry implementation risks. This framing matters because it treats portability and interoperability as competition levers rather than only privacy rights. (OECD)

Recent OECD work also discusses how fast-moving digital markets can generate competition harms before traditional enforcement completes, and it highlights the complexity of digital value chains and the reluctance of dependent firms to cooperate in investigations, which fits the broader story of dependency and chilling effects. (OECD)

Measurement can be concrete. Build a portability score for sellers and users: how many clicks and how much data loss occurs when exporting data, moving catalogs, transferring reviews, migrating customer communications, or switching analytics and ad histories. Then measure whether higher portability correlates with higher multi-homing and stronger price competition. Separately, examine innovation incentives by tracking category-level entry and churn, time-to-imitation patterns, and the relationship between platform observability and seller investment. (OECD)

Falsifiers again help. The data-moat story weakens when portability is real and widely used, when sellers can maintain customer relationships across channels without heavy loss, and when innovators capture durable returns that justify investment even in highly observable categories.

Key terms

- Data portability, the ability to move data between services, reducing lock-in (OECD)

- Interoperability, systems working together so switching and multi-homing remain viable (OECD)

- Lock-in, switching costs driven by trapped data, history, and workflows (OECD)

- Multi-homing, using multiple platforms, a key condition for contestability (OECD)

- Learning advantage, superior market information from platform vantage point, shaping imitation incentives (ONE MP)

- Appropriability, the innovator’s ability to capture returns from innovation, driving investment incentives

WHY THE TEXTBOOK PROMISE DOESN’T SHOW UP AUTOMATICALLY

A free market is supposed to turn private ambition into public benefit through a simple loop:

- Firms try to earn extra profit

- Extra profit attracts entry

- Entry increases supply

- Supply forces better deals, and

- Over time the extra profit melts into lower prices, better service, and more choice.

That loop is why people defend markets, it is a machine for consumer gains.

In real life, the loop depends on three conditions that people forget to check.

- Customers need to be able to compare and switch without effort that feels irrational

- Sellers need to be able to reach demand without paying tolls that erase their cost advantage, and

- Entrants need to be able to scale enough to scare incumbents.

When any of these conditions weaken, the market can stay busy while pressure fades, pricing becomes polite, visibility becomes rented, and sellers become cautious because the map feels more dangerous than the competitor.

So the value of this article is not outrage, it is clarity. You can look at a market and ask three questions, does price respond, can people switch, can newcomers grow. If the answer is yes, you are watching competition do its job. If the answer is no, you are watching a market that performs competition without delivering the usual consumer gains.

THE POCKET DEFINITION OF A FREE MARKET

A free market is a system where a better deal can win. When a business finds a cheaper way to operate, it can cut price and customers can reach it, and rivals must respond. Over time, the extra profit that comes from being unusually efficient or unusually lucky attracts entry, and the consumer receives the gains through lower prices, better quality, and more choice. (OECD)

Modern platform markets still deliver real convenience and trust, and they also introduce new levers that can soften this pressure:

Hidden price floors, gagged routing, default power, rented shelves, engineered switching friction, bundled tolls, self-preferencing, and trapped data.

The practical test stays simple. Look for price discipline, easy switching, and credible entry. If those three show up, the market behaves like a market. If those three fade, the market behaves like a well-designed hallway that always leads you to the same door.

APPENDIX A — GLOSSARY

This glossary exists so readers can follow the argument without feeling like they need an economics degree. Each term has a plain meaning and a “why it matters” sentence.

- Economic profit, profit after including opportunity costs; this is the “profit goes to zero” concept in competitive long-run equilibrium. (OECD)

- Pass-through, the share of a cost or fee change that appears in consumer prices, a central test of competition. (OECD)

- Multi-homing, use of multiple platforms by buyers or sellers; it keeps markets contestable. (OECD)

- Switching costs, time/effort/loss involved in moving to a rival; higher costs soften competition. (OECD)

- Tying and bundling, linking products so complements become harder for rivals to sell; sometimes efficient, sometimes foreclosing. (OECD)

- Self-preferencing, discriminatory routing that favors the platform’s own offerings in ranking/defaults. (Bruegel)

- Data portability and interoperability, technical and policy levers that reduce lock-in and support multi-homing. (OECD)

- Choice architecture, how interfaces present options; it changes effective demand and competitive outcomes. (OECD)

APPENDIX B — ONE-PAGE DIAGNOSTIC SCORECARD

If you want a quick test, use this scorecard. Each line is a yes/no question, and each has one metric you can measure.

- Hidden price floor: Do lower-fee channels show meaningfully lower total prices for identical items over time. (OECD)

- Anti-steering: Can sellers directly communicate and link to alternative routes at the decision moment. (OECD)

- Default gate: Does gaining/losing default placement create a conversion cliff holding value constant. (OECD)

- Pay-to-play shelf: Does ad intensity rise just to maintain sales, and does sponsored placement displace organic comparison. (OECD)

- Switching friction: Is exit measurably harder than entry, and does higher friction correlate with higher markups. (OECD)

- Mandatory add-ons: Do sellers adopt the platform’s complements despite cheaper alternatives, correlated with placement. (OECD)

- Self-preferencing: Do integrated offerings receive systematic placement advantages after controlling for value. (Bruegel)

- Data moat: Is portability low and multi-homing rare because data and reputation do not move cleanly. (OECD)